UAE Insurance Claims for Pharmacies: A Practical Guide to Daman, Thiqa, and NextCare

Insurance claims sit at the centre of UAE pharmacy economics. For most pharmacies in Dubai and Abu Dhabi, claims represent 70 to 90 percent of monthly revenue. Get this right and your cash flow is steady. Get it wrong and you fight rejections, chase outstanding balances, and watch margin disappear into operational overhead.

This guide explains how UAE pharmacy insurance claims actually work in practice. We’ve structured it around what new pharmacy owners and operators most often get wrong, and how the right software can take eighty percent of the friction out of the process.

Why Insurance Claims Matter More in the UAE Than in Most Markets

Three things make UAE pharmacy claim management particularly demanding.

The first is the size of the insured pool. Abu Dhabi made health insurance mandatory in 2008. Dubai followed in 2014. From January 2025, the federal government extended mandatory health insurance to all private sector employees and domestic workers across the Northern Emirates. Roughly 2.5 million additional residents joined the insured pool through the basic AED 320 annual scheme alone. Walk-in cash sales have become the smaller share of pharmacy revenue, not the larger one.

The second is the variety of payers. A typical UAE pharmacy deals with at least 10 to 20 insurance networks and TPAs, each with its own claim format, pre-authorisation rules, and rejection patterns. The market for third-party administrators alone reached USD 430 million in 2025 and continues to grow.

The third is digital infrastructure. Dubai operates eClaimLink, the centralised electronic claims platform run by Dubai Health Insurance Corporation. Abu Dhabi runs Shafafiya through the Department of Health. Federal claims data flows through the Riayati layer for many flows. Pharmacies that try to handle all of this through manual workflows or generic software fall behind quickly.

The UAE Insurance Landscape Pharmacies Actually Deal With

Insurance claims involve three layers, and pharmacy owners often confuse them.

Insurance companies underwrite the policy. Daman, ADNIC, Sukoon (formerly Oman Insurance), Salama, Orient, AXA (now GIG), MetLife, Cigna, and Allianz are all insurers. They take the premium and bear the risk.

Third-party administrators (TPAs) process claims on behalf of insurers. The major TPAs in the UAE include NextCare, NAS Neuron, MedNet, Inayah, Almadallah, MaxCare, GlobeMed Gulf, FMC Network, IRIS Health, MSH International, and Vidal Health. Many TPAs are owned by or affiliated with insurance companies. Most pharmacy claims actually go through a TPA rather than directly to the insurer.

Government health programmes sit alongside private insurance. Thiqa covers UAE nationals in Abu Dhabi (administered by Daman). Enaya covers Dubai government employees and citizens. SEHA Prime serves Abu Dhabi public sector groups. These programmes have their own rules, approved drug lists, and claim formats.

For a pharmacy, this means signing up with the right mix of payers depends on your location, customer base, and partnerships. A pharmacy in Mussafah serves a different population from one in Dubai Marina, and the insurance partners that drive your revenue should reflect that.

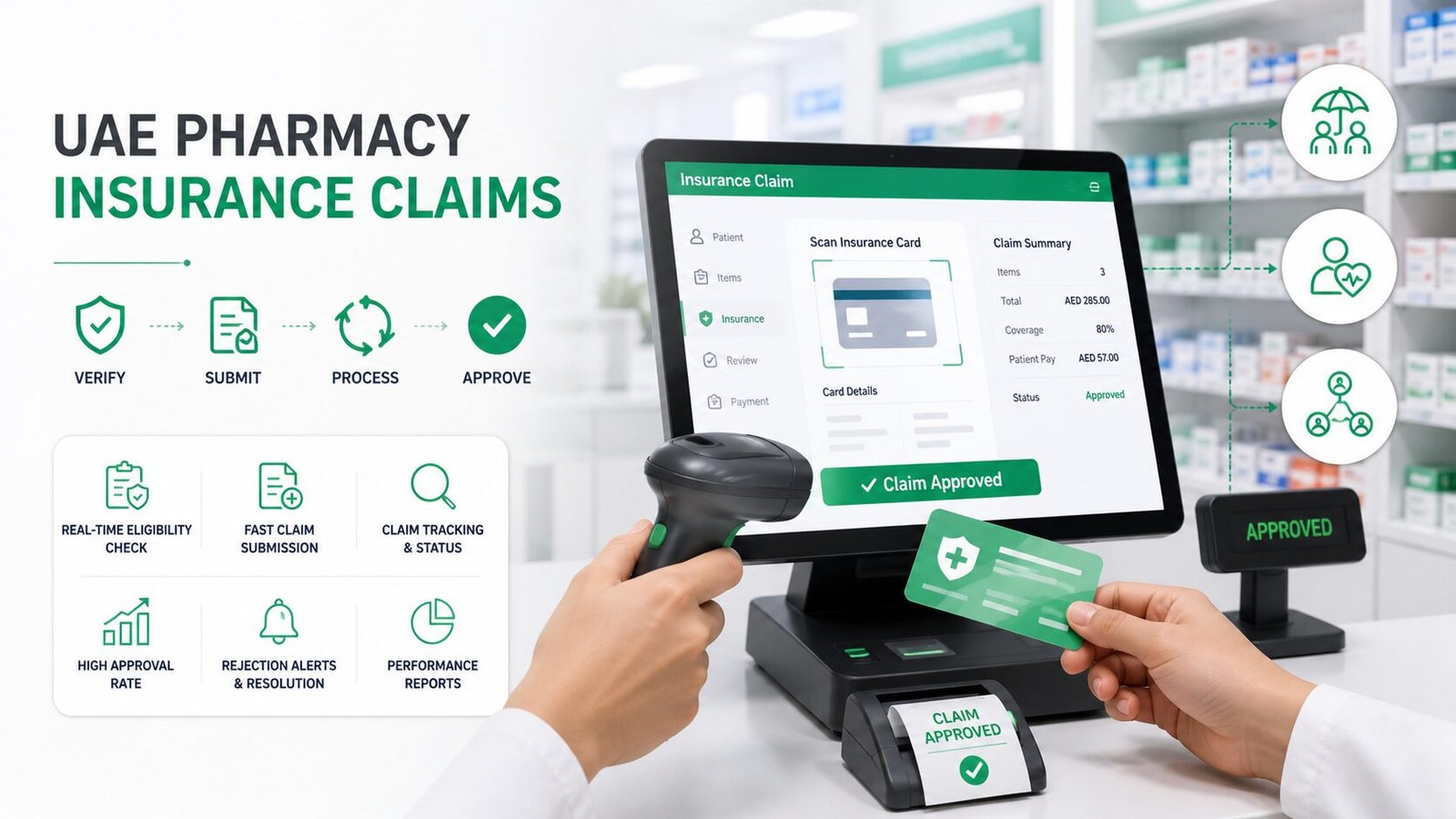

How a Pharmacy Insurance Claim Actually Works

The claim process for most prescription dispensing has six steps.

- Patient presents prescription and insurance card. The pharmacist verifies the card is active, captures the policy number, and checks scheme eligibility through the relevant TPA portal or integrated software.

- Eligibility and coverage check. The system checks whether the prescribed medicine is covered, whether co-payment applies, and whether prior authorisation is needed for that medicine and dose.

- Pre-authorisation request (if required). For chronic medication, high-cost drugs, or specific therapeutic categories, the pharmacy submits a pre-authorisation request to the TPA. The TPA approves or rejects within minutes to hours. Without this approval, dispensing the medicine means absorbing the cost.

- Dispensing and patient co-payment. The pharmacy dispenses the medicine. The patient pays any co-payment in cash or card. The remainder becomes a claim.

- Claim submission. The pharmacy submits the claim electronically through eClaimLink (Dubai), Shafafiya (Abu Dhabi), or directly to the relevant TPA portal. Each payer has its own format and required fields.

- Adjudication and settlement. The TPA processes the claim and either approves it for payment, rejects it, or requests additional information. Payment cycles vary from two weeks to 90 days depending on the payer.

The pharmacist sees only the front end. The software handles formats, validation, and submission rules behind the scenes. When the software is good, this is invisible. When it isn’t, every claim becomes manual work.

The Most Common Reasons Claims Get Rejected

Rejection rates of 8 to 15 percent are typical in UAE pharmacies running average software. Top operators with strong systems push that down to 2 to 4 percent. The gap between average and good is mostly down to avoiding common rejection causes.

Eligibility issues. Patient policy expired, dependent not on the policy, scheme terminated, card flagged. Software that checks eligibility live before dispensing prevents most of these.

Pre-authorisation missing or incorrect. Pharmacist forgot to request authorisation, or requested it for the wrong dose or duration. Strong software flags pre-authorisation requirements automatically and blocks dispensing until approval is in place.

Drug not covered or off-formulary. The prescribed medicine is not on the patient’s covered drug list, or a specific brand is not approved while a generic is. Software that validates against each payer’s formulary catches this before dispensing.

Diagnosis code mismatch. The diagnosis on the prescription does not align with the dispensed medicine according to the payer’s clinical rules. Catching this requires software that understands payer-specific clinical edits.

Quantity exceeds policy limits. The prescription quantity exceeds the maximum per claim or per period for that drug. Limits vary by payer and patient scheme.

Duplicate claim or refill too early. The same medicine was dispensed too recently. Software with claim history checks prevents these.

Format or data field errors. Required field missing, wrong code format, or invalid identifier. These are pure software problems that should never reach a human pharmacist.

The pattern across all of these: most rejections are preventable at the time of dispensing if the software does its job. Software that submits whatever the pharmacist enters and lets the TPA reject it is the most expensive option you can choose.

Building Strong Claim Workflows

A pharmacy that wants insurance claims to support rather than drain operations needs three workflow disciplines.

Live eligibility verification before dispensing. If your software cannot verify policy status and coverage at the point of sale, you are running blind. This is the single highest-impact upgrade most older pharmacies can make.

Automated pre-authorisation tracking. Every requested authorisation should be logged, tracked, and visible to dispensing staff. Authorisation that expires before dispensing is a real and frequent revenue leak.

Daily claim reconciliation. Submitted claims, accepted claims, rejected claims, and pending claims need to be visible every morning. Pharmacies that reconcile weekly or monthly miss the window to fix rejections inside payer time limits.

A pharmacy chain handling claims across multiple branches needs all of this consolidated under one system. Branch-by-branch reconciliation makes a chain pharmacy easier to defraud, slower to spot trends, and harder to negotiate with payers when contract renewal time comes around. We cover this side of operations in detail in our guide to multi-branch pharmacy management in the UAE.

Pre-authorisation: The Most Common Operational Pain Point

Pre-authorisation deserves its own section because it causes more confusion than any other part of the claim process.

Different payers require pre-authorisation for different drug categories, different costs, and different chronic conditions. A medicine that needs no authorisation under Daman might need full authorisation under MedNet for the same patient. Authorisation that is valid for 30 days under one scheme might be valid for 24 hours under another.

The right software handles this by maintaining payer-specific rules per drug, prompting the pharmacist when authorisation is needed, submitting the request through the correct channel, tracking status until approval or rejection, and storing the approval reference against the eventual claim.

Without this, your team spends hours per day chasing authorisations manually, and missed authorisations turn into rejected claims that you absorb as losses.

Claim Aging and Cash Flow

Even approved claims take time to pay. Typical payment cycles in the UAE:

- Major TPAs (NextCare, MedNet, NAS Neuron): 30 to 60 days

- Daman direct claims: 30 to 45 days

- Smaller insurers and private TPAs: 45 to 90 days

- Government schemes (Thiqa, Enaya, SEHA): 30 to 60 days, but variable

A pharmacy with strong claim management runs a “days sales outstanding” of 30 to 45 days. A pharmacy with weak claim management can sit at 75 to 100 days, which means a meaningful share of working capital is locked up in receivables that cannot pay rent or restock inventory.

Aging reports broken down by payer, by claim status, and by branch are essential for spotting which payers need to be chased and which are systematically slow.

What to Look For in Pharmacy Software for UAE Insurance Management

When you evaluate vendors, the questions worth asking are:

- Which UAE insurance networks and TPAs does the software integrate with directly?

- How does eligibility verification work at the point of sale?

- How are pre-authorisation requirements flagged and tracked?

- What rejection reason analytics are built in?

- How do payment cycles and aging reports work?

- For multi-branch operations, are claims and reconciliation consolidated?

- Are claim formats updated automatically when payers change requirements?

We cover the broader feature evaluation in our guide to the 10 must-have features for UAE pharmacy software, and the regulatory context behind claim formats in our pharmacy software compliance guide.

How Pharmasolo Handles UAE Insurance Claims

Pharmasolo handles the major UAE insurance networks and TPAs natively. Eligibility verification runs at the point of sale before dispensing. Pre-authorisation requirements are flagged automatically per drug and payer. Claims submit through the correct channel for each payer. Rejection patterns surface in dashboards so owners can spot which payers and which branches are running into trouble. Multi-branch operations consolidate into a single claim management view.

This was built through years of running pharmacy operations across the GCC through our Pharmasolo platform, and the UAE version inherits all of that with the added local integrations the market needs.

If you’re evaluating pharmacy software for a UAE pharmacy, our buyer’s guide to pharmacy management software in Dubai walks through how to compare options fairly.

Frequently Asked Questions

What is the difference between an insurance company and a TPA?

An insurance company underwrites and bears the risk of the policy. A TPA processes claims on behalf of one or more insurance companies. Most UAE pharmacy claims actually go through TPAs rather than directly to insurers.

Which TPAs do UAE pharmacies most commonly work with?

NextCare, NAS Neuron, MedNet, Inayah, Almadallah, MaxCare, GlobeMed Gulf, and FMC Network handle the largest share of UAE pharmacy claim volume. The right mix depends on your location and customer base.

How does eClaimLink work?

eClaimLink is Dubai’s centralised electronic claims platform, run by Dubai Health Insurance Corporation. Pharmacies in Dubai submit insurance claims through eClaimLink rather than directly to each individual payer. Software that integrates with eClaimLink simplifies claim submission for Dubai operations.

What is Shafafiya?

Shafafiya is Abu Dhabi’s centralised claims data hub, operated by the Department of Health. Abu Dhabi pharmacies submit claim data to Shafafiya for monitoring and reporting purposes.

What is a typical pharmacy claim rejection rate in the UAE?

8 to 15 percent for pharmacies on average software. Top operators using strong claim management software run rejection rates between 2 and 4 percent.

How long does it take for an approved claim to be paid?

Typical payment cycles range from 30 to 90 days depending on the payer. Major TPAs and government schemes generally pay within 30 to 60 days. Smaller insurers and TPAs sit at the longer end.

Is pre-authorisation always required?

No. Pre-authorisation rules vary by payer, drug, and patient scheme. Chronic medication, high-cost drugs, and specific therapeutic categories usually require pre-authorisation. The software should flag this automatically per payer and per drug.

Take Control of Your Pharmacy’s Insurance Operations

Insurance claims are too central to UAE pharmacy economics to leave to weak software. Choosing the right system for claim management is one of the highest-leverage decisions a pharmacy owner makes.

If you’d like to see how Pharmasolo handles UAE insurance networks, eligibility verification, pre-authorisation, and claim aging in a real pharmacy environment, book a Pharmasolo demo for your UAE pharmacy and our team will walk you through it live.